BELIEVE IT OR NOT, there is a plausible path to a $10,000 an ounce Gold Price And it doesn't require a breakdown in civil society

.

Speculators

see central bankers as modern-day superheroes, able to push markets

around with a single phrase. In the minds of most investors, Ben

Bernanke, Mario Draghi and Masaaki Shirakawa might as well be wearing

tights, masks and capes. These superhero central bankers continuously

swoop down into the financial markets to defend them from

downticks...and to insure that they always deliver capital gains.

The

reality, of course, is that these superheroes are frauds. They have no

superpowers...other than the power of mass delusion. The powers of Mario

Draghi and the other central bankers in Europe are waning. Excess debt

is like kryptonite: Each new wave of printing has less impact on

markets. As the popular phrase goes: "This is a solvency problem, not a

liquidity problem."

In other words, new money supply cannot restore health to sick loans and government bonds. The only way to restore solvency to the system is

to deflate the economy or slash the amount of debt in the system

through mass bankruptcy.

Or is there another way? Is there a

"reset button" that central bankers can push (with the approval of

political leaders) that would restore balance to the system?

We know central bankers would never want to deflate the economy or crash the value of debt, which would destroy the banking system. So how about inflating the money supply to dilute the value of debt? All in one fell swoop?

Right

now, central bankers are diluting the value of debt very slowly by

pushing interest rates below the rate of inflation. Some call this

"financial repression." It's an unspoken policy that has many negative

consequences. What is an alternative, since all attempts to "fix" the

current system with more borrowing and printing are failing?

How

about the classical gold standard, which stands out as the least flawed

of all the systems we've tried. Each nation could choose to peg its

local currency to gold at a price that allows for enough growth in bank

reserves to greatly reduce the burden of public- and private-sector

debts.

Re-pegging a currency like the US Dollar to gold at the

current price (about $1,550) has its pitfalls. Most notably, it would

not deleverage an overleveraged banking system. But re-pegging the

Dollar to something like $10,000 an ounce might do the trick.

Hedge

fund managers Lee Quaintance and Paul Brodsky from QB Asset Management

wrote a fascinating outline on the potential reintroduction of gold into

the monetary system, while simultaneously implementing what one might

consider a debt jubilee. QB explains the mechanics of how it could work

in the US:

Using the US as an example, the Fed would purchase

Treasury's gold at a large and specified premium to its current spot

valuation. The higher the price, the more base money would be created

and the more public debt would be extinguished. An eight-to-10-fold

increase in the Gold Price

via this mechanism would fully reserve all existing US

Dollar-denominated bank deposits (a full deleveraging of the banking

system)."

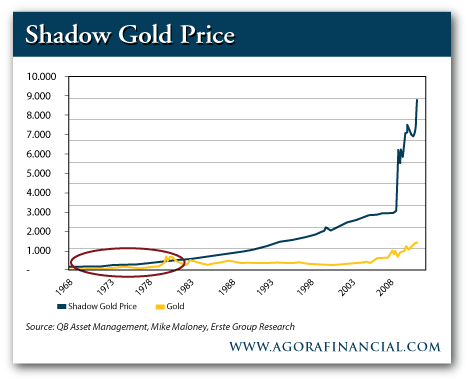

Below is what the remonetization of gold would look like

in chart form. The yellow line would rapidly approach the blue line.

And the blue line will keep rising as we see further growth in the money

supply. QB's "Shadow Gold Price"

divides the US monetary base by official US gold holdings.

Policymakers, who always feel the need to manage something, would

appreciate that this is the same formula used during the Bretton Woods

regime to peg the Dollar at $35 per ounce. In other words, the Shadow Gold Price

is the theoretical price of gold after the Fed inflated the supply of

Dollars to a level that would cover systemic bank liabilities and then

re-pegged the Dollar to gold. Behold the path to $10,000 gold:

This

path would weaken the economy-sapping effects of debt created since

President Nixon closed the gold window. It would transform a debt-based

currency into an asset-backed currency. No longer would one ask the

unpleasant question "What backs the Dollar?" and come away with even

more questions (and a headache). Right now, the Dollar is backed by

Treasuries held on the Fed's balance sheet, which are in turn backed by

Dollars, which are in turn backed by faith in fiat money — i.e.,

nothing!

QB's monetization scenario would impose losses on certain

parties as the reset button is hit, but unlike most of the policy

prescriptions we've seen lately, it seems to solve more problems than it

creates. Most notably, politicians could argue that this reset would

involve "migration of value, in real terms, from leveraged assets to

unleveraged goods, services and assets." Wage earners would be winners

relative to asset owners, because "stable to higher nominal asset prices

would require even higher nominal wage and consumable pricing looking

forward."

This scenario argues for holding some shares in

producers of physical commodities (especially gold miners), even if it

feels like we're in a deflationary environment. A gold standard, after a

one-time debt monetization, would make for a more-balanced, efficient

global economy less prone to violent booms and busts.

As an added

bonus: Central bankers would no longer be viewed as superheroes! Just

meager servants, pegging the money supply to gold and letting the free

market determine the price of money. After all, when in history has

central planning worked better over time than the free market?

We

can hope the central bankers of the world stumble their way to a

solution like that proposed by QB Asset Management before they inflict

even more damage to the foundation of the global economy. Unfortunately,

conditions may have to get much worse in financial markets, banking

systems and economies before such "outside the box" ideas are

considered. A defensive portfolio with exposure to gold and other real

assets seems like the right mix in today's environment.

Give us a call for all of your precious metals needs at 801.889.7200 or online at valleygoldminesaltlake.com